Learn how to set clear financial goals and achieve them with smart planning, budgeting, saving, and investing strategies. Build financial discipline and long-term success.

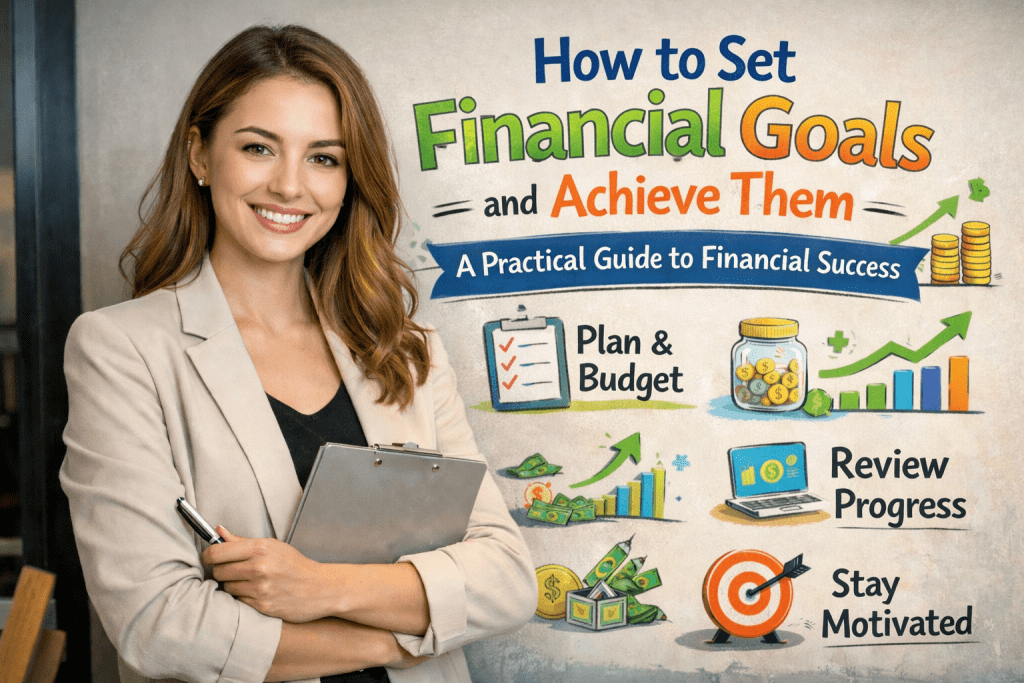

Setting financial goals and achieving them is one of the most powerful skills you can develop for long-term success and peace of mind. At its core, financial goal setting is about giving your money a clear purpose instead of letting it disappear on random expenses. Whether your aim is to save for education, buy a home, eliminate debt, build an emergency fund, or achieve financial independence, everything starts with clarity. You must first understand where you currently stand financially by reviewing your income, expenses, savings, and debts. This honest self-assessment acts like a financial mirror—it shows what’s working and what needs improvement. Once you know your starting point, you can define specific and realistic goals. Vague ideas like “I want to be rich” or “I want to save money” are not effective; instead, goals should be clear, measurable, and time-bound, such as saving a certain amount within a specific period or paying off a loan by a particular date. Clear goals give direction and make progress easier to track.

After setting clear financial goals, the next crucial step is to break them down into manageable actions. Large goals can feel overwhelming, but when divided into smaller steps, they become achievable. For example, if your goal is to save $6,000 in a year, breaking it down into monthly or weekly savings targets makes it far less intimidating. This is where budgeting plays a vital role. A well-planned budget helps align your daily spending with your long-term goals. By categorizing expenses and identifying areas where you can cut back, you free up money to allocate toward your goals. Budgeting doesn’t mean depriving yourself of enjoyment; rather, it’s about making intentional choices. Even small adjustments, like reducing impulse purchases or dining out less frequently, can significantly accelerate progress over time. Consistency in following your budget is what turns plans into results.

Read Also: Top Financial Mistakes That Are Costing You Money and How to Avoid Them

Another key factor in achieving financial goals is building strong saving and investing habits. Saving should be treated as a non-negotiable expense—something you pay yourself first before spending on anything else. Automating savings can be especially helpful, as it removes temptation and ensures regular progress without requiring constant effort. For long-term goals, investing becomes essential because it allows your money to grow through compound interest. Starting early, even with small amounts, can make a dramatic difference over time. While investing may seem intimidating at first, learning basic concepts and choosing simple, low-risk options can help you build confidence and stay committed. The combination of consistent saving and smart investing creates momentum that brings your financial goals closer every day.

Staying motivated and disciplined is often the biggest challenge in achieving financial goals. Life is unpredictable, and unexpected expenses or changes in income can slow progress. This is why flexibility and regular review are so important. Revisiting your goals monthly or quarterly allows you to track progress, celebrate small wins, and make adjustments when necessary. An emergency fund also plays a crucial role here, as it protects your goals from being derailed by sudden financial shocks. Equally important is maintaining the right mindset. Financial success is rarely about quick wins; it’s about patience, perseverance, and long-term thinking. Mistakes may happen, but learning from them instead of giving up keeps you moving forward. By staying focused, adapting to challenges, and consistently aligning your daily financial decisions with your long-term vision, you can turn your financial goals into lasting achievements and build a stable, confident financial future.

Achieving financial goals also requires developing self-control and emotional awareness around money, which is often overlooked but incredibly important. Many financial setbacks happen not because of low income, but because of emotional spending—buying things to cope with stress, boredom, or social pressure. Learning to pause before making financial decisions can make a huge difference. Asking simple questions like, “Does this move me closer to my goal?” or “Is this a want or a need?” helps you stay aligned with your priorities. Over time, these small moments of mindfulness build strong financial discipline. Creating visual reminders of your goals, such as progress charts or written affirmations, can also keep motivation high, especially during moments when giving up feels tempting.

Another powerful strategy for achieving financial goals is increasing your income alongside managing expenses. While budgeting and saving are essential, there is a limit to how much you can cut costs. Exploring ways to grow your income—through side hustles, freelancing, skill development, or career advancement—can significantly speed up your progress. Investing in yourself by learning new skills or improving existing ones often leads to higher earning potential in the long run. When extra income is directed intentionally toward financial goals instead of lifestyle inflation, it becomes a strong accelerator for success. This approach not only helps you reach goals faster but also builds confidence and a sense of financial control.

Accountability is another key element that supports long-term success. Sharing your financial goals with a trusted friend, family member, or mentor can help you stay committed. Accountability doesn’t mean giving up privacy; it simply means having someone who encourages you to stay on track and reminds you of your purpose when motivation dips. Some people also find success by tracking progress publicly through journals or digital tools, which adds an extra layer of responsibility. Regularly reviewing your progress—monthly or even weekly—helps you identify what’s working and what needs adjustment. These check-ins turn goal-setting into an active process rather than a forgotten plan.

Finally, it’s important to recognize that financial goals evolve over time, and that’s perfectly normal. As your income, responsibilities, and life priorities change, your goals should change too. What matters most is building a system that supports smart financial decisions at every stage of life. Setting financial goals is not a one-time task; it’s a lifelong habit that grows stronger with experience. By staying intentional, adaptable, and consistent, you create a strong financial foundation that supports both your present needs and future dreams. In the end, achieving financial goals isn’t just about money—it’s about gaining freedom, confidence, and the ability to design a life on your own terms.